Award-winning PDF software

Us tax year Form: What You Should Know

IRC 7805. [4] Rev. Pro. 2002-39 provides the general procedures for taxpayers not within the scope of either Rev. Pro. 2002-37 or Rev. Pro. 2002 IRS Considerations for Establishing an Annual Business Cycle or Seasonal Business, IRC § 1.4507(a)(2)(A). Rev. Run. 2002-1. C.B. 1045, provide for an annual accounting period of 3 years for certain taxable years (see IRC section 7703, which defines a taxable year for purposes of the annual business cycle test). 2002-24, 2004-1 I.R.B. 639. §1.4507. Change of annual business cycle test. (a) Definition. For purposes of the annual accounting period test, the term “annual business cycle” means the same time period as is defined in paragraphs 2(b) and 2(c) of section 1202(a) of this title (relating to periods for which income is taxed); see §1.4533-2(c) (relating to definitions). (b) No testing under this section for taxable years beginning before January 1, 2002. No testing under this section for taxable years beginning on or after January 1, 2003. IRC §§ 1.4515(a)(6) and 1.4515-6. Subchapter B — New Rules and Regulations Subchapter B Chapter 1 — Business of Partnerships; Provisions for Transfer of Assets and Partnership Statuses Rev. Pro. 2002-39, I.R.B., 2002-39, § 1.1.10-14) New provisions regarding a partnership's transfer of assets. Rev. Pro. 2002-39, I.R.B., 2002-39, § 1.1.11-28) Provisions for transfer by a partnership from one taxable year in which an asset is held by the partnership to a taxable year for which it holds a different asset. Rev. Pro. 2002-39, I.R.B., 2002-39, § 1.1.34-9] The term “transfer” means the creation or acquisition of an interest in an asset by making a transfer of shares of stock, or an interest in an entity by issuing securities as provided by this section. Rev. Pro.

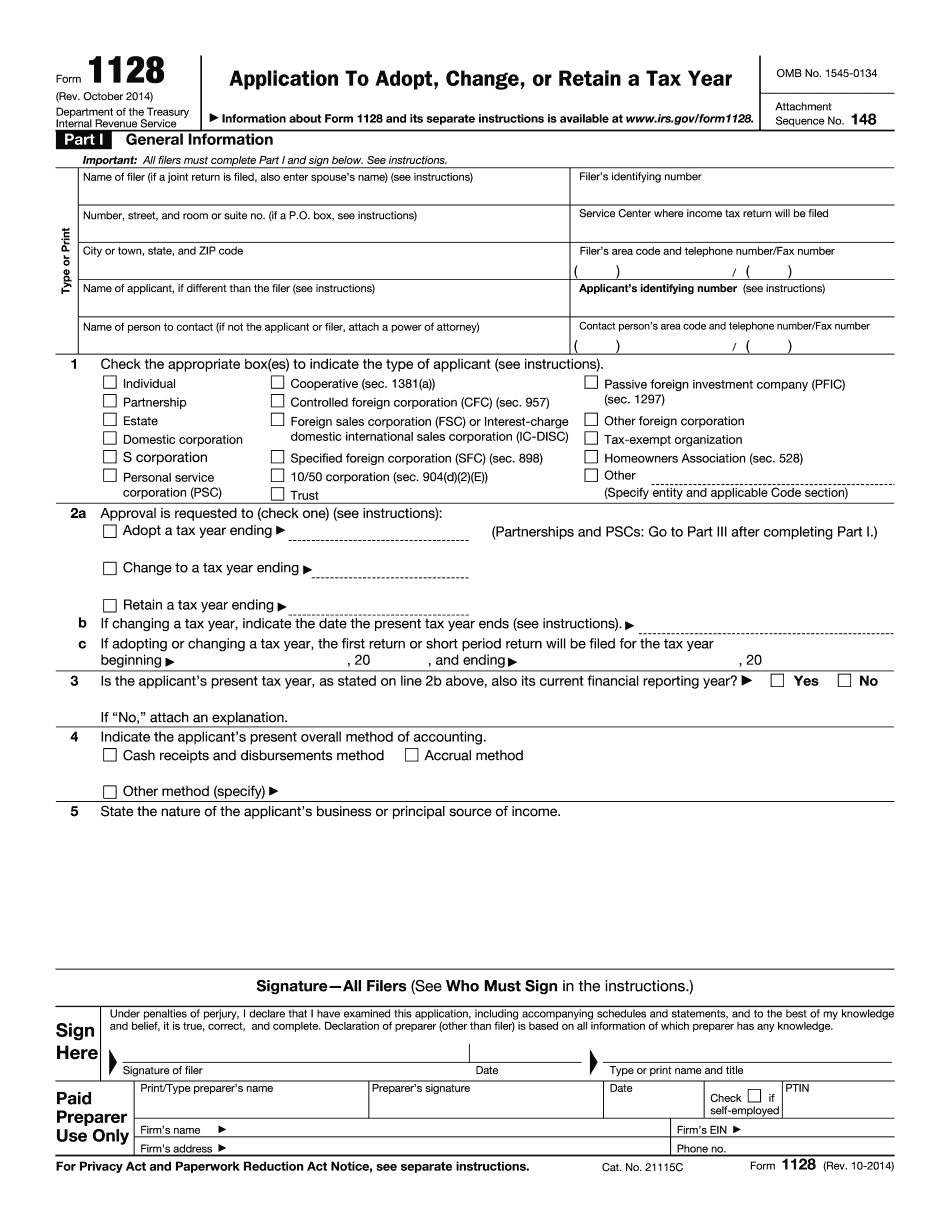

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1128, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1128 Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1128 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1128 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.